Jurisdictions

Regions

Industry Sectors

07/04/21

Rapid Growth Of Sustainable Finance Plays To IFC Strengths But Will Make A Jurisdiction’s Reputation Critical

It’s time to treat sustainable finance as the mainstream.

Its transition from a niche in the charitable, development, and quasi-governmental realms to the industry-wide norm is well and truly underway; where it is not, such a transition is both inevitable and imminent. It is encouraging to see many in international finance centres – such as Jersey Finance – taking a lead. But the scale and speed of the change will require substantial engagement and effort by industry, regulators, and governments in IFCs if the new opportunities are to be seized and the challenges addressed.

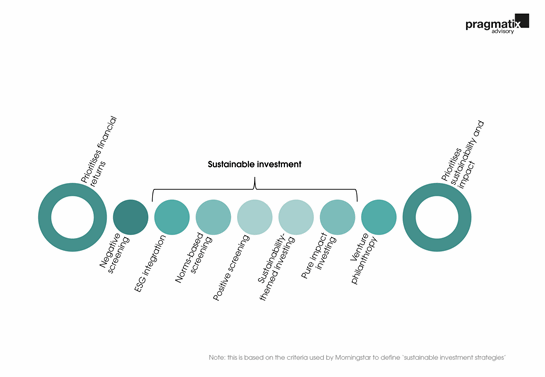

In our research and modelling work in this space to date, we take sustainable finance to include all those investment and financing activities that purport to focus on the integration of environmental, social and governance (ESG) criteria, norms-based screening, positive screening and/or sustainability themes linked to the United Nations’ Sustainable Development Goals, as well as pure ‘impact investments’. It is a wide and heterogeneous spectrum.

Definitions of sustainability are both numerous and ambiguous. This makes putting a precise number on the size of the market for sustainable finance at any one point in time nearly impossible. Conservative estimates by the International Finance Corporation suggest that more than US$3.8 trillion (and up to US$12.5 trillion) of assets were invested sustainably in 2019. On a broader definition this figure is well in excess of US$30 trillion.

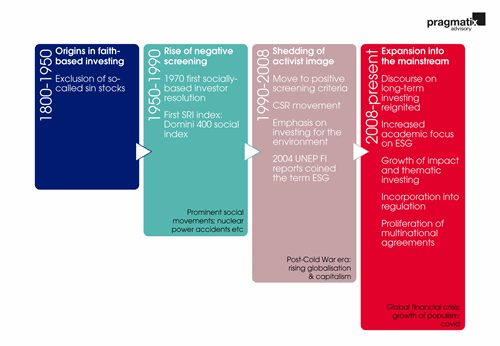

On any chosen definition, the types of investment that can be described as sustainable are diverse. Historically, sustainable investing was simply about ‘negative-screening’ i.e. the exclusion of certain types of companies from investment mandates. By and large, such investment strategies were a simple box-ticking exercise in compliance. Investors were too-often reluctant participants rather than engaged proponents.

This is no longer the case; across the investment community there is active consideration of non-financial impact as well as pecuniary returns. For the industry, including those in IFCs, non-financial sustainability is an increasingly important element of fiduciary duty.

Although currently dominated by European investors, the next decade will see root and branch change. Where Europe has led, the United States and elsewhere will quickly follow and overtake.

In coming years, sustainable will become the new mainstream as non-sustainable investments become untenable due to changing investor and regulator values and improved financial performance. On reasonable assumptions, the global sustainable fund market could grow to almost fifty times its current scale by 2030 – although the bulk of this will be through existing businesses changing to conform to new standards rather than through the formation of new assets.

Despite increasing growth rates in recent years, this remains a substantial step up from recent years, albeit one that we believe to be plausible. The precise future trajectory is far from clear. We are wary of placing too much stock in the historical trends of what remains a relatively young market. In our recent report, ‘Making more than money’, we have developed a range of scenarios that could see anywhere from US$9.5 trillion to US$70 trillion in sustainable funds by 2030. Regardless, either side of this range represents a remarkable expansion of the market.

This strong growth derives from the accumulation of several structural changes.

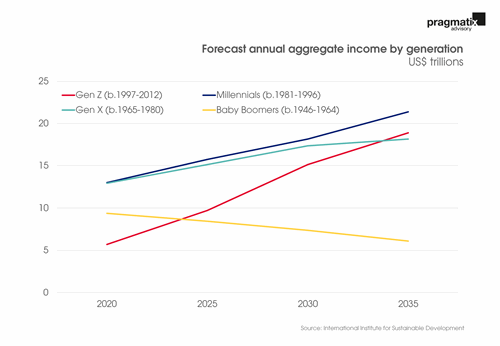

First, a new generation of socially and environmentally aware investors are in the process of bringing sustainability-related values directly to their investment activities. Aided by the large and ongoing intergenerational wealth transfer from older generations to millennials, this is likely to go a long way towards making sustainability the norm.

Second, political and institutional attitudes to sustainability are changing with increasing attention being paid to international and domestic targets and policies. There is growing pressure being put on companies and investors to report on the impacts of their activities. Today, ESG reporting is a specific requirement for companies listed on many stock exchanges around the world including the Nasdaq, Euronext, and the Shanghai, Hong Kong and London Stock Exchanges. The United Kingdom’s intention is to make non-financial disclosures mandatory across the economy by 2025, with a significant portion in place by 2023. The European Union’s Sustainable Finance Action Plan aims to reorient capital flows towards sustainable investments, mainstream sustainability into risk management, and increase transparency and long-termism in financial and economic activity. Across the Atlantic, the United States’ multi-year struggle over climate change disclosure seems to be coming to a head, with the Securities and Exchange Commission recently announcing a comprehensive review of disclosure requirements.

These additional regulatory measures mean that compliance with sustainability standards is becoming a critical part of the finance industry’s licence to operate.

Third, in the context of widespread COVID-related disruptions to supply chains and travel, debate on key environmental and social issues has been reignited. This has helped to reset perceptions in favour of sustainability and inspired calls for a ‘green recovery’ to ‘build back better’. Looking forward, we expect this to be accelerated as both public and private sectors prepare for the 26th United Nations Climate Change conference (COP26) in November.

Of course, targets, pledges and promises to find sustainable alternatives do not always translate to action, especially if such alternatives are to come with hefty price tags attached. And all this before we consider those cases where there are no suitable sustainable substitutes for a particular form of finance.

Why, then, are we so bullish about growth in sustainable finance? The answer lies in its now proven potential to provide strong financial returns on par with more conventional equivalents.

This time last year, when many investments were hit hard by the pandemic, sustainable investments thrived. Covid has reinforced that sustainable investments can provide strong financial returns to investors. Several studies have found that sustainable investments outperformed their peers during the initial market sell-off and throughout 2020.

Much of this strong performance can be explained by factors that combine to make these investments less volatile and more resilient during market downturns. After all, sustainable investments tend to be made in companies that have strong governance practices and generally exclude investments in resource-intensive sectors such as oil and other extractives.

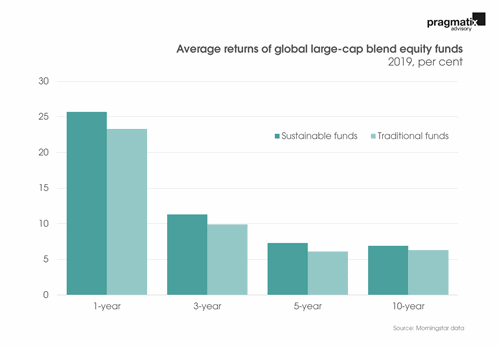

Yet even in more stable market contexts, sustainable investments are profitable for those seeking strong financial returns. In terms of both success rates and average returns, sustainable investors need pay little or no premium when compared with their non-sustainable peers. According to Morningstar data, a majority of sustainable funds have outperformed their traditional peers with 59 per cent beating their average traditional counterpart over the decade to 2019. Over one- and three-year time periods, this figure rises to 66 per cent. Sustainable global large-cap blend equity funds have seen annual returns more than half a percentage point higher than similar traditional funds over ten years to 2019.

Sustainable funds also perform better when it comes to their relative survival rates over different time scales. This is encouraging because it suggests that strong average returns are not purely a result of survivorship bias and that these funds are able to stand the test of time.

The growth in and mainstreaming of sustainable investment provides opportunities for IFCs.

It is inherently more international. The challenges of climate change and international supply chain ethics are distinctively global issues. With more investments made in pursuit of sustainability goals, a growing share will be concentrated in markets outside of Europe and North America. Cross-border financial expertise will be increasingly relevant and needed. Moreover, the speed with which the market is growing and changing will play to a strength of many offshore centres: innovation and adaptability.

But, as the market for sustainable finance grows, increasing attention will be paid to the way that IFCs communicate their sustainability credentials.

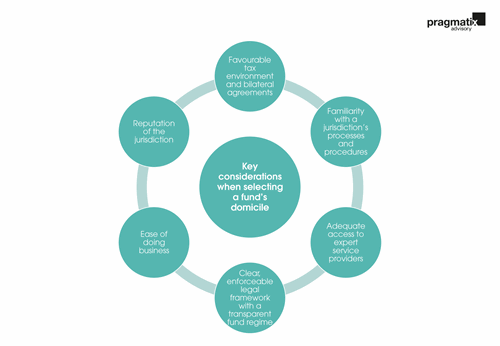

When selecting where to domicile a company or fund, managers traditionally consider multiple factors including tax efficiency, costs, economies of scale and the ability to implement their investment strategy. While these considerations are also important for sustainable fund managers, assessments of trust, transparency and credibility tend to play more prominent roles in the decision process.

Familiarity has historically offered incumbent jurisdictions a competitive advantage. However, IFCs must not rely on the inertia of investors and their intermediaries. We expect clients to demand more of jurisdictions on the sustainability front. Alignment of jurisdictional and investor values is gaining momentum and successful IFCs will pre-empt and respond to these trends rather than wait to play catch-up.

Reputation will carry more weight as priorities move away from the clear financial metrics of cost and return towards more complex objectives around fulfilling mission. Beware ‘greenwashing’ – or being caught doing it. And, in this environment, tax will likely become an even greater issue. Sustainable investments already tend to carry a relatively high share of public monies by way of development finance institutions and national governments. But private contributors will likely be more sensitive to negative publicity around taxation.

Despite lacking a clear common language and measurement standards, investors and regulators are increasingly demanding more information about the complete impact of investments. As a result, any strategy that forgoes transparency is unlikely to pay-off in the long run.

For IFCs, the sustainable investment market offers an unrivalled opportunity for a reputational and branding reset – and to tap into strong growth and new clients. But this new normal world will likely be less forgiving of ambiguous ethics and reputational own goals. Move quickly but tread carefully.

Clare Leckie

With a focus on impact investment and environmental projects, Clare contributes to the full range of Pragmatix Advisory’s assignments, especially those requiring detailed and methodical quantitative analysis and modelling. She holds a BA in philosophy, politics and economics from the University of Oxford, and is studying for an MSc in economics and policy of energy and the environment at University College London.

Mark Pragnell

Mark Pragnell, director of Pragmatix Advisory, has over 25 years’ experience as a macroeconomics consultant and forecaster. He has worked with a number of IFC governments, promotional bodies and businesses, and has led seminal research to explain and quantify the value of IFCs.

Sevra Rende

Sevra is an associate of Pragmatix Advisory and founder of Otrera Advisory. She has over ten years of experience assisting clients around the world understand markets, develop business strategies, and evaluate transactions. She was business development executive and senior economist at Capital Economics where she assisted major asset managers with investments through bespoke due diligence. Prior to that, she spent several years specialising in the energy business at IHS Markit and in economics at the Economist Intelligence Unit. Sevra holds MSc in International Business (Economics) from University of Lancaster and with a BA in Business Administration in Management from Anadolu University in Turkey.