Jurisdictions

Regions

Industry Sectors

05/01/24

BEPS 2.0: Milestones Of Progress In 2023

As we enter 2024, it is good to take stock of where we are now on the BEPS 2.0 project. One can divide BEPS 2.0 into four elements, some of which are interrelated. They are: • Pillar 1 Amount A, which is a reallocation to market jurisdictions of profits, broadly comprising 25 per cent of profits above 10 per cent, for MNEs with revenue above €20 billion. Related to this is an agreement to hold back the proliferation of Digital Services Taxes and relevant similar measures. • Pillar 1 Amount B, which seeks to find a standard methodology for the determination of mark-ups on basic marketing and distribution rights. • Pillar 2 Global Minimum Tax at 15 per cent for MNE groups with revenue in excess of €750m. • The Subject to Tax Rule which provides an opportunity for countries to lift the effective tax rate on certain cross-border transactions to 9 per cent through changes to the treaty rules between two countries.

Pillar 1 Amount A & Digital Services Taxes

On 11 October 2023, the OECD released a substantial body of work that reflects two years of negotiation. This included a near final Multilateral Convention to Implement Amount A of Pillar One referred to as the ‘MLC’. It comprises 53 articles of 90 pages, plus nine annexes of 130 pages and an Explanatory Statement of nearly 640 pages. There is also a separate 23-page document explaining several processes for obtaining tax certainty. In addition, there is a new analysis of the financial impacts of Amount A.

The release of this package led to the US Treasury Department announcing a consultation process under which comments from the public were requested by 11 December 2023. This process will help to inform the views of the US Administration and Congress on Amount A.

Importantly, an agreement on 12 July 2023 provided for the extension into 2024 of a ‘standstill’ of the proliferation of Digital Services Taxes (DSTs) and relevant similar measures on the condition that at least 30 jurisdictions covering at least 60 per cent of the ultimate parent entity jurisdictions of in scope MNEs signed the MLC before 31 December 2023. Given the significant number of in scope MNEs from the US, the conditions for the extension of the standstill agreement would be unlikely to be met if the US did not sign. Treasury Secretary Janet Yellen was reported in the press as stating that the US would not sign the MLC in 2023.

Thus, the standstill agreement on DSTs will not be extended into 2024 unless it were to be renegotiated. This may mean that some jurisdictions will proceed to implement or reignite DSTs in 2024. Generally, this will take time given legal and parliamentary processes in most jurisdictions.

The acceptance of Amount A in the US is far from certain, both in terms of whether it will be embraced or when. By way of contrast, the EU has been supportive of proceeding with Amount A as has the rest of the world, although India, Brazil and Colombia have made reservations on some aspects of the MLC as drafted.

What is new in the MLC from previous expectations arising from the consultation process? There are two additional exclusions to Extractives and Regulated Financial Services. They involve defence industries and domestic oriented businesses. The latter could apply where there are minimal differences between where revenue is sourced under the rules and where they would be reallocated under the Amount A mechanism. There is a new methodology for calculating a Marketing and Distribution Safe Harbour which is designed to ensure that there is not double taxation in a market jurisdiction. There has also been a resolution (subject to India, Brazil and Colombia’s reservation) of the issue of whether withholding taxes should be taken into account in determining the profit to be allocated to market jurisdictions. There are also many definitions that have been tightened.

One observation is that the Inclusive Framework has sought to design rules that have significant depth and are not simply a determination of principles or, for the most part, reliant on an analysis of facts and circumstances without guidance.

Pillar 1 Amount B

Amount B is an attempt to simplify the application of transfer pricing rules to baseline marketing and distribution activities. It provides for standardised returns between an operating margin of between 1.5 per cent and 5.5 per cent depending on the industry of a distributor, the operating asset and operating expense intensity. It applies to wholesale distributors of tangible goods, irrespective of size or profitability. There are certain adjustment mechanisms proposed for jurisdictions with higher credit risk which is used as a proxy for business risk.

Amount B applies to all companies, not simply those over a certain size, and will be introduced though a change in the OECD Model Transfer Pricing Guidelines.

Amount B has been though a number of consultation processes, the most recent concluding at the beginning of September. We are expecting a further document on Amount B early in 2024. This may constitute the final new guidelines or a step towards such finalisation.

There appears to be a number of responses from jurisdictions in relation to Amount B. Low-capacity developing jurisdictions tend to be strongly supportive of the proposal as do jurisdictions with MNE that face significant disputes. Some jurisdictions expect or demand high returns for marketing and distribution rights and tend not be supportive.

One critical question is whether Amount B will be a safe harbour or made compulsory. There are variations of this theme such that the rules may be mandatory for MNEs operating in low-capacity jurisdictions.

It is possible that Amount B will become a reference point for Tax Administrations rather than provide a direct tool for transfer pricing disputes.

Pillar 2 – GloBE Rules

These are the rules for a global minimum tax of 15 per cent. This is calculated using Model Rules developed by the Inclusive Framework released in December 2021 and for which we have had Commentary in 2022 and two tranches of Administrative Guidance in 2023, in addition to certain Safe Harbour Rules and an outline of the GloBE Information Return.

We are expecting additional guidance on CBCR-based Safe Harbours early in 2024 in addition to guidance on the granularity required on what are termed as the ‘Deferred Tax Liability’ recapture rules.

It is expected that 2024 will give rise to additional guidance on many other topics.

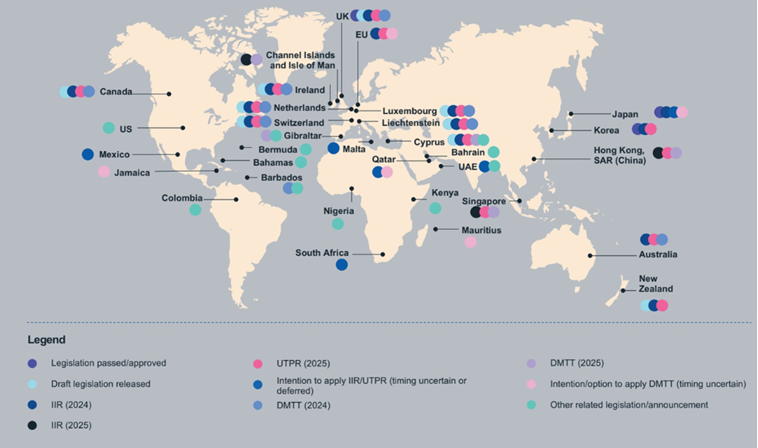

Implementation Of The GloBE Rules

A European Directive required implementation for EU Countries of GloBE Rules by 31 December 2023. This covers the Income Inclusion Rule for financial years on or after 1 January 2024 and the UTPR similarly from 2025, with optionality allowed for the Qualified Domestic Minimum Top-up Tax (QDMTT). The European Directive allows for countries with twelve or fewer in scope MNEs to defer the introduction of the GloBE rules until 2030. Five member states have indicated they will do so. They are Estonia, Latvia, Lithuania, Malta and Slovakia. A significant number of EU countries have either issued draft legislation or the legislation is going through their parliamentary processes. A large portion of the EU countries are introducing QDMTT rules from 2024.

The UK has enacted legislation on the GloBE rules. It was the earliest jurisdiction to do so, and the passage of legislation preceded certain additional guidance from the OECD which is likely to give rise to further tranches of legislation. Norway, Switzerland and Liechtenstein are also embracing the GloBE rules.

The Asian region is characterised by two waves. In the 2024 wave, there is Japan and Korea which have enacted law, and Australia and New Zealand in the process of doing so. In a 2025 wave lies Hong Kong, Singapore, Malaysia, Thailand and Vietnam.

China, India and Indonesia are yet to make formal announcements, but it is likely that they will join a 2025 wave or possibly later.

Canada is proceeding with the GloBE rules with the release of draft legislation and an application from 2024. The Bahamas, Bermuda and Barbados are in various stages of consultation on implementation of a domestic minimum tax either framed as a QDMTT or otherwise.

Latin American has been slower to pick up the initiative at the domestic level, although Columbia has introduced a 15 per cent minimum tax. Various jurisdictions in Africa and the Lower Gulf are considering the GloBE rules.

Subject To Tax Rule (STTR)

On 2 October 2023, the Multilateral Instrument was open to jurisdictions to sign. There is however a significant process such that the likely earliest effective date for implementation of the STTR is likely to be 2026. Under the STTR, developing countries can require updates to treaties, either through the MLI or bilateral negotiations where the adjusted nominal rate falls below nine per cent. The adjusted nominal rate looks at the statutory rate and makes adjustments for income that is preferentially treated.

The income covered is interest, royalties, distribution rights, insurance and reinsurance, guarantee fees, and payments for the use of equipment. Significantly, income for the provision of services is also covered. However, capital gains is not covered, although it was requested by a number of developing countries.

The rules contain anti-avoidance back-to-back rules which will require care in implementation.

What’s Next?

The beginning of 2024 is likely to see releases on Amount B and further guidance on the GloBE rules, particularly in respect of the operation of the CBCR-based safe harbour.

Throughout 2024 we expect additional guidance.

In parallel, we will see an increasing number of countries enact legislation, most of which will be part of a 2024 wave, but in Asia a 2025 wave will be influential.

Jurisdictions will commence processes on the Subject to Tax Rule.

Significant focus will be on the US reaction to Amount A and the potential increase in DSTs.

Pillar Two: State of Play. December 2023.

Grant Wardell-Johnson

Grant is a Global Tax Policy Leader at KPMG, specialising in base erosion and profit shifting and tax policy and planning. Grant joined KPMG in 1987 and became partner in 1997. He has led a number of high-profile IPOs, acquisitions and transactions for major multinational organisations.